Financial statements contain different reports and disclosures telling the readers about the financial situation of a company.

Due to the amount of information that can be found within financial statements, every company and business professional should know how to read financial statements and understand them.

The income statement is a report that catches the attention of most readers since everyone is interested in knowing how much money a company makes. It gives a good insight into the profitability of an entity.

Below, we will dig a little deeper into the income statement, we will provide explanations on what it is, how it works and what’s in the income statement.

Income Statement: Explained

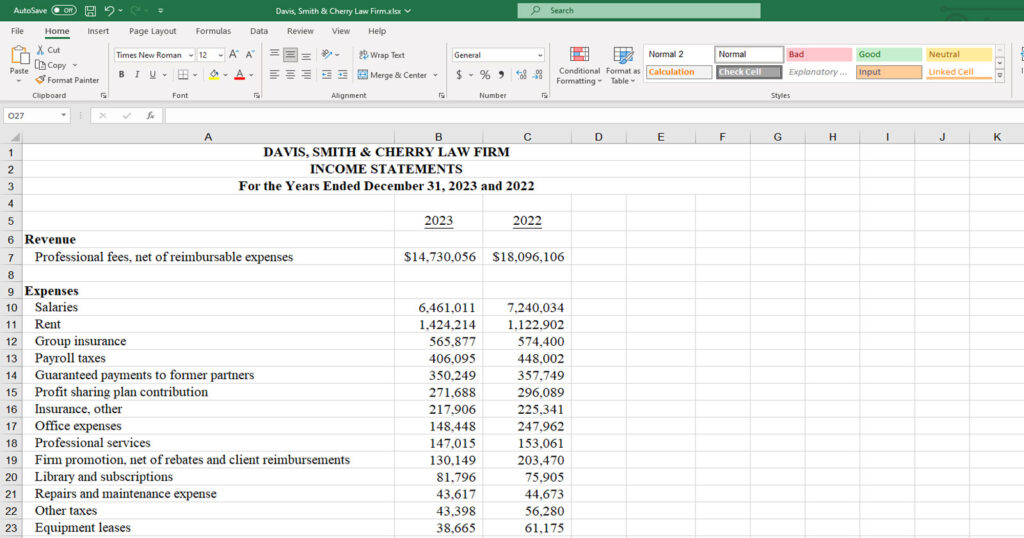

In accounting, the income statement is considered one of the main reports included in the financial statements, along with the balance sheet and the cash flow statement. On the income statement, we can find information about the income, expenses and gains or losses of an entity.

Unlike the balance sheet where the information is presented for a specific date, the income statement presents the activity of a specified period, usually the financial period pre-determined by a company.

With the revenues section, you can see what a company generates from its operating activities. In the expenses section, you can understand how much a company needs to spend in order to generate revenues from its operational activities.

There’s also a gains or losses section where you can see the performance of any investments made by the company.

For finance professionals, an income statement is a good source of information to understand how a company operates, what it generates and what are its expenses.

Compared to other companies in the same industry, an income statement can let the readers understand the operations and management’s performance.

For management, it also helps to understand what generates the most revenue in a company or what expenses are highest in order to adjust production or try alternative options to decrease costs.

Income Statement: How Does It Work?

An income statement shows the performance of a company and its net earnings. An important formula to remember about the income statement :

NET INCOME = REVENUES – EXPENSES +/- GAINS/LOSSES

In practice, it isn’t uncommon to see different subtotals in the income statement. For example, a common subtotal is presented after the operational revenues less expenses to show the net income from operations of the company only.

To get to the net income, let’s also not forget about income taxes. Another popular subtotal happens before the tax expenses, which is the income before taxes. It really depends on what the company wants to show or what kind of information is most interesting for the investors.

Read More:

The Most Important Financial Reports for Small Businesses

The Income Statement: What’s In It?

We learned the fundamental formula behind the income statement. Now let’s take a deeper look into what’s in the income statement. Specifically, what revenues, expenses, gains or losses are made of.

Keep in mind that there are differences between different industries but we will lay out the fundamentals.

Revenues can be split between operating revenue and non-operating revenue.

- Operating revenue: This relates to income generated by the principal activities of a company. For instance, a retail company or manufacturer has the main purpose of selling products.

Therefore, any revenue generated by the sale of their products will be included in the operating revenue. For an insurance company selling insurance coverage, their operating revenue would be income generated by the insurance premiums. - Non-operating revenue: This relates to any income generated by the company that is not directly related to its main operational activity.

For example, if a retail company invests in stocks or bonds and receives dividends or interest income, those would be included in the non-operating revenue.

Similarly, if a manufacturer or an insurance company has invested in rental properties and receives rental income, that would be considered non-operating revenue.

Expenses, just like revenues, are also split into two types; operating expenses and non-operating expenses.

- Operating expenses: This relates to any cost necessary in order to generate an operating sale.

The most popular categories are cost of goods sold, employee salaries, amortization, sales commissions and any administrative expenses directly related to the operations of the company. - Non-operating expenses: This relates to any expense incurred for non-operational activities. For example, if a company obtains a bank loan and pays interest, the interest expense could be included in the non-operational expenses.

Gains or losses:

This section includes any gains or losses generated from non-operational activities such as the sale of fixed assets or any other type of long-term assets.

For example, if a company sells its old or unused equipment, the gains or losses generated by those types of transactions would be included in gains or losses. Generally speaking, the gains and losses are not recurring every year and are generated by specific events.

Recap on The Income Statement in Accounting and Final Thoughts

The income statement paints a great picture of a company’s performance over a period of time. It presents the revenues, expenses and gains or losses of a company. To get to the net income, we simply subtract the expenses from the revenues, add any gains and remove any losses.

An income statement is overall an important tool for finance professionals to evaluate whether a company is profitable or not.